If you’re selling in Westchester and heading to Connecticut, timing can make or break the move. You may be trying to unlock equity from your current home, line up a down payment, and avoid ending up between homes for a few weeks. The good news is that with a strong plan, you can reduce a lot of that stress. Here’s how to think through the sale, the purchase, and the in-between steps before you list.

Why timing matters now

Westchester County was a seller’s market as of February 2026, with 1,482 homes for sale, a median listing price of $660,000, and a median of 44 days on market, according to Realtor.com’s Westchester County market overview. Homes were also selling for about 100% of list price on average.

For you, that can be helpful on the sale side. It also means your move plan should be ready before your home goes live, especially if you need your Westchester proceeds to buy in Connecticut.

Sell first or buy first?

For many homeowners, selling first is the cleaner path. The Consumer Financial Protection Bureau notes that people who are moving commonly try to sell their current home before buying another one.

That sequence often makes the most sense when your down payment for Connecticut depends on the sale of your Westchester property. It gives you a clearer budget, reduces the chance of carrying two homes at once, and can lower financing pressure during the move.

When selling first makes the most sense

Selling first is usually the safer choice if:

- You need sale proceeds for your Connecticut down payment

- You want to avoid two mortgage payments at the same time

- You prefer shopping with a firm budget instead of an estimate

- You want a stronger position when making offers on Connecticut homes

In a market where Westchester homes are moving relatively quickly, this plan can be easier to manage than trying to buy first and hope your current home sells on time.

What to know about buying in Connecticut

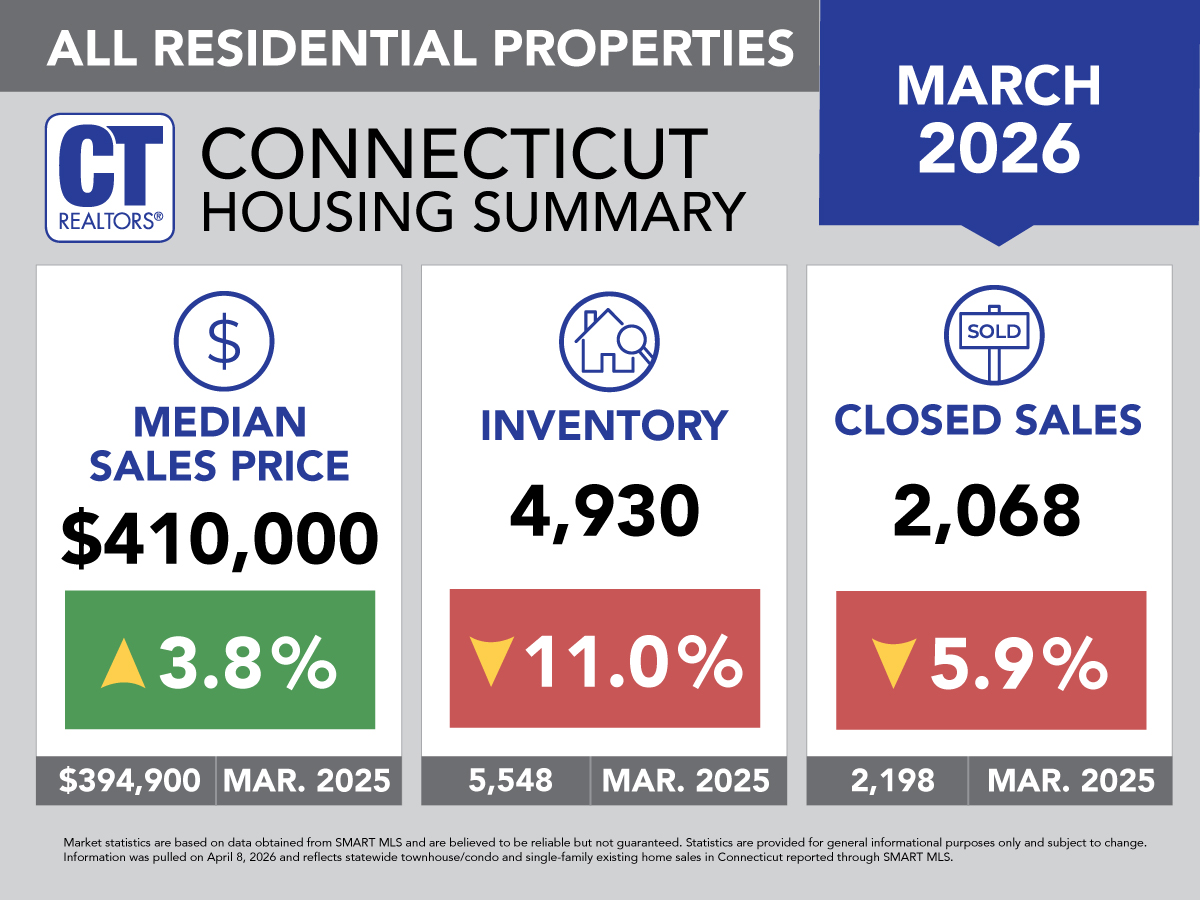

Connecticut may look more affordable than Westchester at a statewide level, but pricing can vary a lot by town. CT REALTORS’ March 2026 statewide housing summary reported a median sales price of $410,000, while Realtor.com’s Connecticut market page showed a median listing price of $450,000 and 36 median days on market.

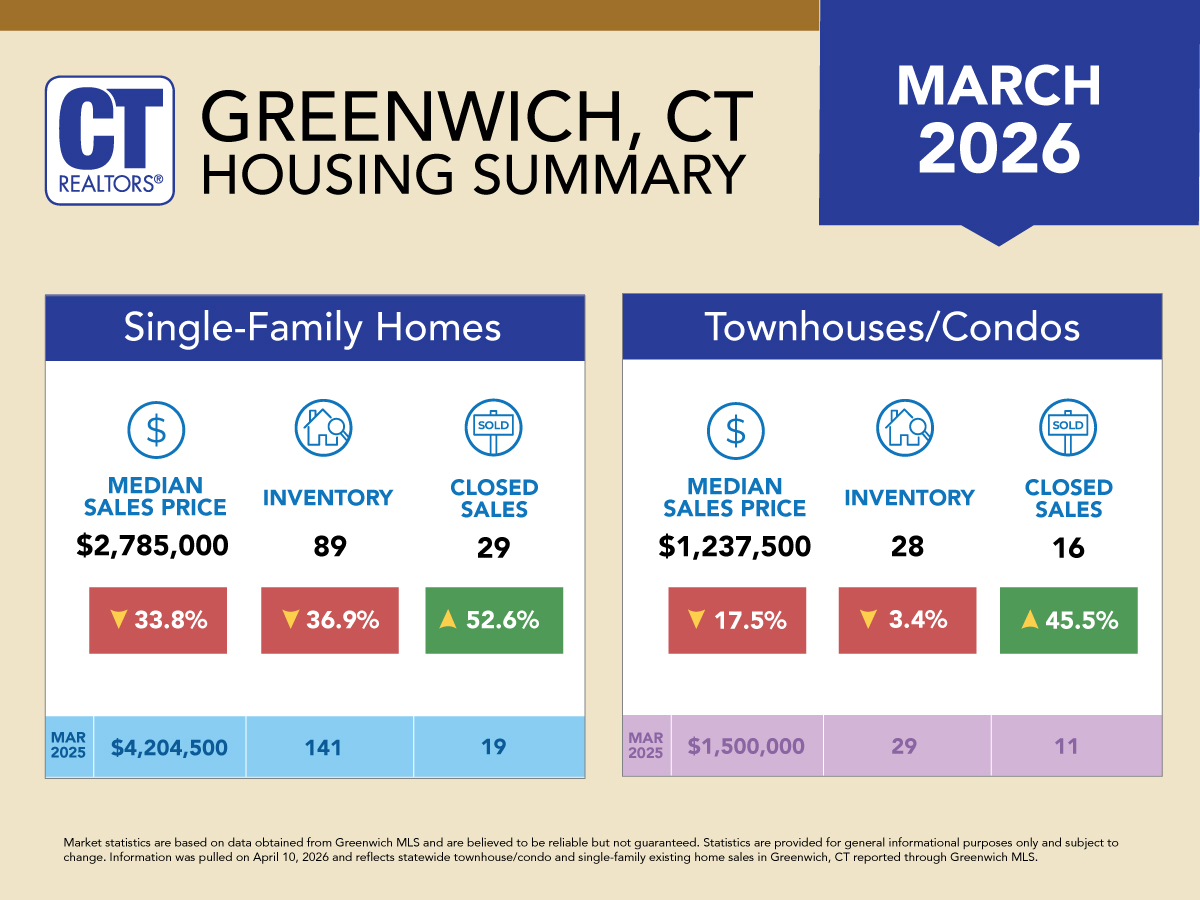

Those numbers suggest Connecticut can offer a lower price point than Westchester overall, but not every town will feel like a discount. For example, CT REALTORS’ March 2026 Greenwich summary shows a single-family median sales price of $2,785,000.

Do not assume all Connecticut towns cost less

This is one of the biggest mistakes movers make. Your Westchester equity may stretch further in some Connecticut towns, but not in every market.

That is why your plan should include:

- A target price range for Connecticut

- A short list of towns you are seriously considering

- A backup plan if your preferred town is more expensive than expected

- A temporary housing strategy if your sale closes before your purchase

Can you make a contingent offer in Connecticut?

Yes, but the type of contingency matters. The National Association of Realtors consumer guide on contract contingencies explains that a home-sale contingency gives you time to sell your current home before closing, while a home-close contingency gives you time to close on your current sale before buying the next home.

If your Westchester home is still on the market, a home-sale contingency may help protect you. If your home is already under contract, a home-close contingency may be a better fit because the sale is further along.

Why contingent offers can be harder

Contingencies reduce risk for you, but they can make your offer less attractive to a seller. NAR also notes that sellers may continue showing the property and may use a kick-out clause if a better offer comes in.

In practical terms, a fully financed, non-contingent offer is often easier to negotiate than a long home-sale contingency. That does not mean a contingent offer cannot work. It just means timing, documentation, and a realistic strategy matter even more.

What if your Westchester home sells first?

This is a common concern, and it is one reason backup housing should be part of your move plan from the start. If your home closes before you secure the right Connecticut property, you still have options.

Option 1: Rent-back after closing

A rent-back lets you stay in your Westchester home for a short period after closing. According to NAR’s guidance on post-closing occupancy, the arrangement should be in writing, insurance should be reviewed, and many lenders do not allow leasebacks longer than 60 days.

This can be a useful tool when your sale must close before your move-out date. It gives you extra time to finish your Connecticut search, complete inspections, or line up your next closing.

Option 2: Temporary housing

Short-term housing can work if your timeline gap is larger or a rent-back is not available. Westchester’s median rent was $3,200 per month, while Connecticut’s statewide median rent was $2,200 per month, based on the market data in the research above.

Even so, rental inventory is limited in both places, so it is smart to start that search early. Waiting until your closing date is near can leave you with fewer choices.

How much of your sale proceeds will you actually keep?

Your sale price is not the same as your net proceeds. Before you count on a certain amount for your Connecticut purchase, make room for taxes, payoff amounts, and closing expenses.

New York transfer tax

New York State imposes a real estate transfer tax of $2 for every $500 of consideration, or 0.4%, on conveyances over $500, according to the New York State Department of Taxation and Finance. The seller usually pays this base tax. The same source also explains that the 1% mansion tax applies to residential purchases of $1 million or more and is generally paid by the buyer.

Mortgage payoff and other closing costs

If you still have a mortgage, that payoff will come out of your sale proceeds at closing. On the purchase side, the CFPB says closing costs typically run 2% to 5% of the purchase price, not including your down payment.

The CFPB also notes that lenders must provide the Closing Disclosure three business days before closing. That short review window is important because it is often when buyers catch fee changes, cash-to-close numbers, or final questions.

Could you owe capital gains tax?

Maybe, but many homeowners qualify for an exclusion. The IRS says you may exclude up to $250,000 of gain, or up to $500,000 on a joint return in many cases, if you meet the ownership and use tests for your main home. The basic rule is explained in the IRS guidance on sale-of-residence tax rules.

If your Westchester property had rental use, an accessory apartment, or business use, the tax picture may be more complicated. The IRS notes that business or rental use can affect how much gain is excludable, so it is wise to review your specific situation with a CPA before you list.

Build your timeline backward

The smoothest cross-state moves usually start with a written plan, not just a target month. Because your Connecticut purchase may depend on your Westchester proceeds, each milestone should connect to the next.

A simple planning sequence

Here is a practical order to follow:

- Estimate your likely Westchester sale proceeds

- Set your Connecticut budget and town list

- Decide whether you need to sell first

- Prepare your Westchester home for market

- Discuss contingency options for your Connecticut purchase

- Line up a rent-back or temporary housing backup

- Watch inspection, appraisal, and closing deadlines closely

This step-by-step approach gives you more control if one piece shifts.

Expect a few moving parts on the Connecticut purchase

Even after your Westchester home is under contract, the Connecticut side can still affect timing. The CFPB explains that buyers generally need both an appraisal and a home inspection, and if the contract is contingent on a satisfactory inspection, the buyer can cancel without penalty if the inspection is unsatisfactory.

That means repairs, inspection findings, or appraisal issues can delay closing or change your plans. A flexible transition strategy is often what keeps the whole move from becoming rushed.

A smart move starts before the listing goes live

Selling a Westchester home before moving to Connecticut is not just about getting a strong price. It is about coordinating equity, timing, housing, and contract terms so your next step feels stable instead of stressful.

If you want clear guidance on the Connecticut side of your move, Yasmina Delacruz-Bailey can help you plan your purchase strategy, evaluate town-by-town price differences, and prepare for a smoother cross-state transition.

FAQs

Should I sell my Westchester home before buying in Connecticut?

- For many homeowners, yes. Selling first is often the cleaner option when you need your Westchester equity for the Connecticut down payment.

Can I make a contingent offer on a Connecticut home while selling in Westchester?

- Yes. A home-sale or home-close contingency may be possible, but contingent offers can be less appealing to sellers than non-contingent offers.

How long can I stay in my Westchester home after closing?

- A rent-back may allow you to stay after closing for a short period, but NAR notes that many lenders do not allow leasebacks longer than 60 days.

Are Connecticut homes always cheaper than Westchester homes?

- No. Connecticut has a lower statewide median price than Westchester, but town-by-town prices vary widely, and some markets like Greenwich are significantly more expensive.

What costs reduce my Westchester sale proceeds before I buy in Connecticut?

- Common reductions include your mortgage payoff, New York transfer tax, and other closing-related costs, which can affect how much cash you have available for your next purchase.

Could I owe taxes after selling my Westchester primary home?

- Possibly, but many homeowners qualify for a capital gains exclusion if they meet the IRS ownership and use tests. Rental or business use can change the tax outcome.

{kind=link}

{kind=link}